7 minute read

7 minute read

Introduction

Most working professionals assume they are already protected against accidents. The logic feels simple.

“I have a premium credit card.”

“My bank provides accident insurance.”

"My employer already has insurance for me. ”

But very few actually read the terms and conditions.

In reality, office insurance, credit card benefits, and bank-linked accident covers are limited. They apply only in specific situations, such as when travel tickets are booked using a particular card. Outside these narrow conditions, coverage may not apply at all.

This is a problem because accidents do not follow schedules. This is where most assumptions around insurance start to fail. They can happen at home, at work, on stairs, near construction sites, or during routine daily life

The risk is compounded by how poorly prepared India remains for accidents. According to the Insurance Regulatory and Development Authority of India, general insurance penetration is about one percent.

This includes personal accident insurance.

It is far below global averages.

These figures appear in the IRDAI Annual Report 2023 to 2024.

Business Standard also reported them. At the same time, India accounts for about 11% of global accident deaths . Yet only about 3% of people have a personal accident policy. This leaves many families dependent on limited coverage from employers, banks, or credit cards.

For professionals and business owners, the real risk is not just injury, but loss of income and long-term earning ability. While health insurance may cover treatment, it does not replace income or support ongoing financial commitments. This is why personal accident insurance for self and family is a core part of financial protection and an essential step in responsible financial planning today.

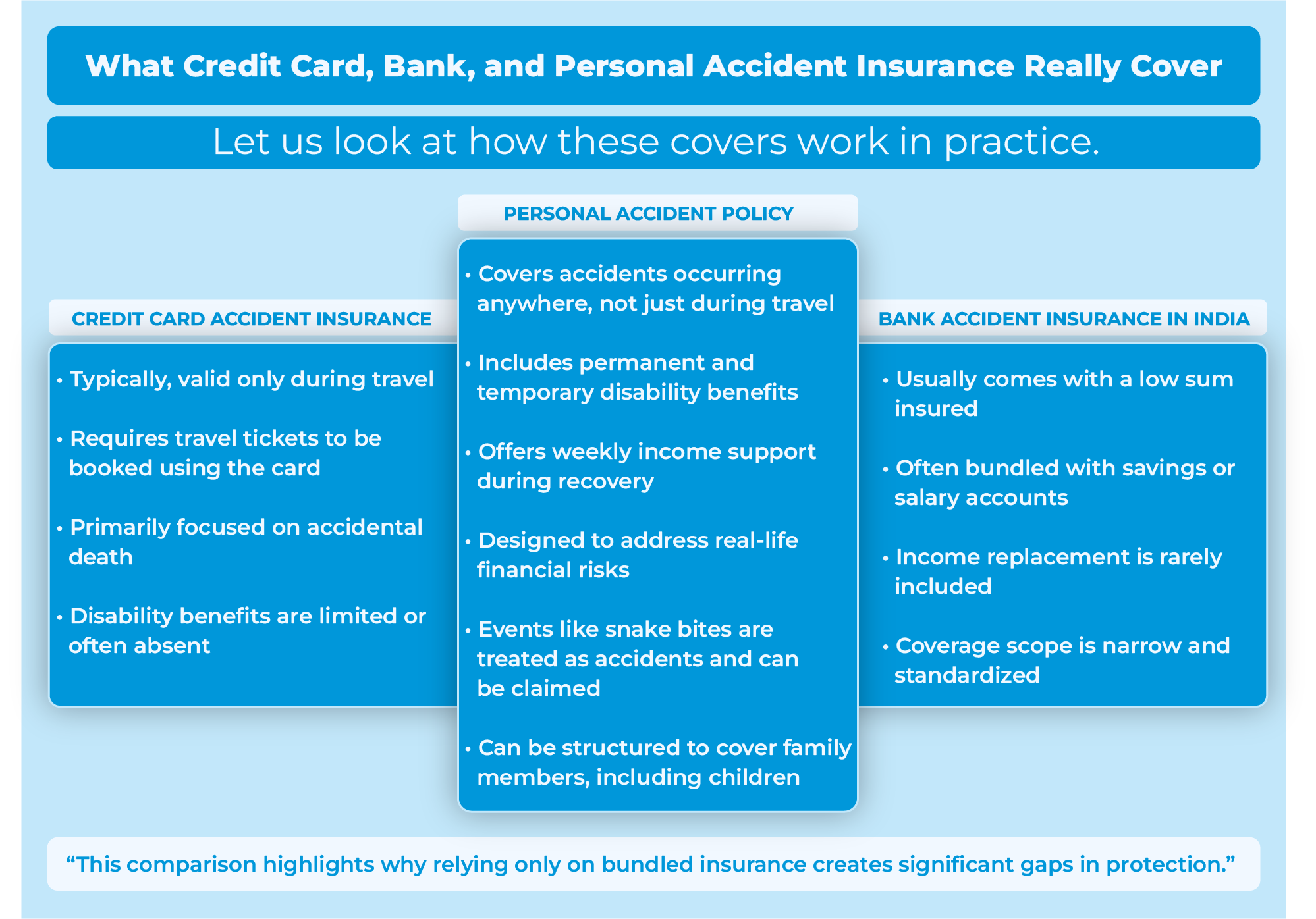

The Common Myth Around Credit Card and Bank Insurance

A large number of professionals rely on bundled insurance benefits without fully understanding what they actually provide. These typically come from three sources.

- Credit card accident insurance

- Bank-linked accident insurance

- Employer or office provided group insurance

The assumption is simple. If accident cover exists through work, a bank, or a credit card, it must be sufficient.

In reality, these covers are designed for convenience and scale rather than individual financial protection. Credit card accident insurance usually applies only when travel tickets are booked using the card and is largely restricted to accidental death during the journey, with little or no disability or income support.

Bank accident insurance in India is often bundled with savings or salary accounts. It usually has low coverage limits and strict conditions. Employer or office-provided group insurance offers similar limitations.

While it can act as a basic safety net, it is non-portable, linked to continued employment, and often does not reflect individual income levels or family responsibilities. A job change or move into self-employment can significantly reduce or eliminate this protection

This directly answers a common question many people search for.

This directly answers a common query:

Does credit card insurance cover accidents?

Yes, but only under specific conditions

Another frequently asked question is.

Is credit card accident insurance valid without a travel booking?

In most cases, no.

The larger issue is that relying on employer, bank, or credit card insurance shifts personal responsibility onto institutions whose coverage is not designed around real-life financial needs. These benefits may offer limited support in specific situations, but they are not built to protect income or family stability after a serious accident. Treating bundled insurance as complete accident protection often leaves significant gaps when support is needed most.

What Personal Accident Cover Actually Means

A personal accident policy protects against the financial impact of accidents, regardless of where or how they occur. It is not linked to travel, specific activities, or transactions such as ticket bookings or bank account conditions.

In simple terms, it provides financial support when an accident affects your ability to earn

A comprehensive personal accident cover typically includes accidental death benefit, permanent and temporary disability benefits, and weekly income support during recovery.

Unlike bundled insurance, a personal accident policy can cover both the individual and their family, including a spouse and children. This makes it a core part of financial protection and a responsibility that rests with the individual, not with an employer, bank, or credit card provider.

Why Personal Accident Insurance Is Important in Financial Planning

Financial planning typically focuses on wealth creation and protection against major medical costs. Investments, tax planning, retirement goals, and health insurance get due attention, but income continuity is often taken for granted.

An accident can disrupt earning ability overnight, and even a short recovery can strain finances as expenses continue despite the loss of income. This is where personal accident insurance becomes critical, helping protect income and financial stability, not just medical costs.

Consider a realistic scenario. 35-year-old professional earning ₹15 lakh rupees annually meets with an accident and is unable to work for eight months

During this period:

- Regular income stops

- Monthly expenses remain unchanged

- Savings may be redirected to manage routine commitments

- Long term financial goals can be delayed or compromised

For business owners and self-employed professionals, the impact can be even more severe. There is no employer salary buffer, and income often stops entirely when work stops.

This is why personal accident cover for income protection becomes essential. It helps replace lost income during recovery and provides financial stability when earning capacity is temporarily or permanently affected.

This kind of situation explains why an increasing number of professionals are asking:

What happens if I become disabled and cannot work in India

A well-structured personal accident cover for income protection in India ensures that your lifestyle and financial commitments remain stable even during recovery.

Key Benefits You Should Not Ignore

Understanding the financial impact of an accident goes beyond medical treatment. A comprehensive accident insurance coverage in India should focus on protecting income, independence, and long‑term stability when the ability to work is affected.

A strong personal accident policy typically includes:

Accidental Death Benefit

Provides a lump sum payout to support the family in case of death due to an accident.

Permanent Total Disability

Ensures income protection if an accident leads to complete and irreversible inability to work.

Permanent Partial Disability

Offers proportionate compensation for loss of function that may reduce earning ability.

Temporary Total Disability

Supports short‑term income loss when recovery prevents you from working.

Disability Benefits

Provides regular income during recovery, helping manage monthly expenses without exhausting savings.

Additional Benefits

Some policies also include hospital cash allowance, rehabilitation support, education support for children, OPD benefits for accident‑related fractures, and coverage for coma‑related treatment.

Together, these benefits ensure accident protection goes beyond survival and helps maintain financial stability and dignity for both the individual and the family.

What Credit Card, Bank, and Personal Accident Insurance Really Cover

Real-Life Financial Risks: What Happens After an Accident

Accidents create far more than immediate medical expenses. In many cases, they lead to sustained financial pressure that continues long after hospital discharge. This reality is often underestimated until a serious accident occurs.

While road accidents receive the most attention, many serious accidents in India occur outside traffic situations. Some of the most common causes include:

- Drowning in and around open water bodies such as ponds, open drains, and swimming pools

- Accidental fires caused by gas leaks, electrical faults, or unsafe cooking practices

- Falls from height, including stairs, rooftops, ladders, or construction sites

- Electrocution due to faulty wiring or exposed electrical connections

These incidents frequently take place at home, at the workplace, near construction zones, or in everyday environments that are often considered safe, reinforcing the need to plan for accident risks beyond the roads..

Drowning remains a leading non-traffic cause of accidental death in India, especially during monsoon seasons and near unsecured water sources. Accidental fires from gas leaks or electrical faults, falls from stairs or construction sites, and electrocution due to faulty wiring frequently result in severe injuries that can permanently affect mobility and earning ability.

In cases of severe trauma or coma, the financial impact escalates quickly. Families may face extended hospitalization, high treatment costs, loss of active income, and emotional stress that intensifies financial pressure.

Coma care and extended recovery can push treatment costs into several lakhs over time. Even when health insurance covers part of the expense, income often stops while household, loan, and education costs continue

This is where a well‑designed personal accident policy becomes critical. It is not just about surviving an accident, but about maintaining financial stability while recovery is still in progress.

How Much Personal Accident Cover Is Enough in India

One of the most common questions working professionals ask is:

Is personal accident cover enough in India

The answer depends largely on your income and financial responsibilities.

A practical way to think about coverage is to link it directly to your earning ability and long‑term obligations:

- Minimum coverage of 10 to 15 times your annual income

- Higher coverage for business owners due to income variability

- Inclusion of a weekly compensation feature

- Comprehensive coverage for both temporary and permanent disability

For example, if your annual income is ₹20 lakh, an appropriate personal accident cover would typically fall in the range of ₹2 crore to ₹3 crore.

This level of protection helps ensure:

- Financial security for your family

- Continuity of income during recovery

- Protection of long-term financial goals

Limitations You Should Be Aware Of

Even the most comprehensive personal accident policies have certain limitations. Understanding these in advance helps set the right expectations and avoids unpleasant surprises during claims.

Common exclusions and conditions typically include:

- No coverage for self-inflicted injuries

- High-risk activities excluded unless specifically mentioned

- Claims subject to defined terms, timelines, and procedures

- Proper and timely documentation is critical for claim settlement

It is also important to remember that a personal accident policy is not a replacement for health insurance. The two serve different purposes.

Health insurance covers medical and hospital expenses.

Personal accident insurance focuses on income loss and the broader financial impact of disability or death.

Together, they form a more complete protection strategy.

How to Choose the Right Personal Accident Policy

Choosing the right personal accident policy requires focusing on coverage quality, not just cost. When evaluating options, pay attention to:

- Comprehensive coverage for both temporary and permanent disability

- Inclusion of a weekly compensation benefit for income support

- A sum insured that is aligned with your income level

- A clear and well-defined claims process

- The overall reputation and claims track record of the insurer

Avoid making the decision based only on the premium. A lower-cost policy with limited coverage may fail to provide meaningful support when an accident occurs.

Conclusion

Relying on employer, credit card, or bank‑provided accident insurance can create a false sense of security. These covers are limited, conditional, and not designed around real‑life financial responsibilities or long‑term income protection.

A well‑structured personal accident cover is a core part of responsible financial planning. It protects your income, supports family stability, and helps ensure long‑term financial goals remain intact when unexpected events occur.

The real question is not whether you have accident cover, but whether your cover is actually enough.

Take the Next Step

If you are currently relying on a credit card or bank insurance, it is worth reviewing your coverage before it is tested in a real situation.

At Harmoney Finserv, the focus is on helping professionals and business owners build structured financial plans that protect income, not just investments. .

Schedule a consultationA simple review today can help you avoid major financial gaps tomorrow.

FAQs

1. What do credit card and bank accident insurance actually cover in India?

In India, credit card and bank accident insurance usually offer limited coverage, such as:

- Accidental death benefit, often only during travel

- Coverage only if tickets are booked using the card

- Minimal or no disability benefits

- No income replacement or weekly compensation

They are not designed for complete financial protection and should not be relied on as your primary cover.

2. Does credit card accident insurance work without booking travel tickets?

In most cases, no. Credit card accident insurance is typically valid only when you book travel tickets using that card. Accidents outside this condition are usually not covered.

3.What does a personal accident cover actually include in India?

A personal accident cover generally includes:

- Accidental death benefit

- Permanent total disability

- Permanent partial disability

- Temporary disability

- Weekly compensation for income loss

This makes it more comprehensive than bank or card-based insurance.

4. How much personal accident cover is enough based on income?

A practical benchmark is 10 to 15 times your annual income. This ensures financial stability for you and your family in case of death or disability.

5. What happens if I become disabled and cannot work in India?

If you do not have proper coverage:

- Your income stops immediately

- Expenses continue

- Savings may get depleted

- Financial goals get disrupted

A personal accident policy helps replace lost income and maintain stability during recovery.

6. Why is personal accident insurance important in financial planning?

It protects your income, which is the foundation of your financial plan. Without it, even a temporary inability to work can impact your lifestyle, savings, and long-term goals.